End-to-End Operators: The Next-Generation Consumer Businesses

7 min read

At Battery, a central part of our consumer-investing practice involves tracking the evolution of where and how consumers find and purchase goods and services. In our research, we’ve seen seismic shifts in how consumer purchasing behavior has changed over the years, starting with the move to the web and, more recently, to mobile and on-demand via smartphones.

The evolution looks like this in a nutshell: In the early days, listing sites like Craigslist, Angie’s List* and Yelp effectively put the Yellow Pages online – you could find a new restaurant or plumber on the web, but the process of contacting them was largely still offline. As consumers grew more comfortable with the web, marketplaces like eBay, Etsy, Expedia and Wayfair* emerged, enabling historically offline transactions to occur online. More recently, and spurred in large part by mobile, on-demand use cases, managed marketplaces like Uber, DoorDash, Instacart and StockX* have taken online consumer purchasing a step further. They play a greater role in the operations of the marketplace, from automatically matching demand with supply, to verifying the supply side for quality, to dynamic pricing.

Each stage of this evolution unlocked billions of dollars in value, and many of the names listed above remain the largest consumer internet companies today.

At their core, these companies are facilitators, matching consumer demand with existing supply of a product or service. While there is no doubt these companies play a hugely valuable role in our lives, we increasingly believe that simply facilitating a transaction or service isn’t enough. Particularly in industries where supply is scarce, or in old-guard industries where innovation in the underlying product or service is slow, a digitized marketplace – even when managed – can produce underwhelming experiences for consumers.

In these instances, starting from the ground up is what is really required to deliver an optimal consumer experience. Back in 2014, Chris Dixon wrote a bit about this phenomenon in his post on “Full stack startups”. Fast forward six years, and more startups than ever are “full stack” or as we call it, “end-to-end operators.”

These businesses are fundamentally re-imagining their product experience by owning the entire value chain, from end-to-end, thereby creating a step-functionally better experience for consumers. Owning more in the stack of operations gives these companies better control over quality, customer service, delivery, pricing and more — which gives consumers a better, faster, and cheaper experience. It’s worth noting that these end-to-end models typically require more capital to reach scale, as greater upfront investment is necessary to get them off the ground than other, more narrowly focused marketplaces. But in our experience, the additional capital required is often outweighed by the value captured from owning the entire experience.

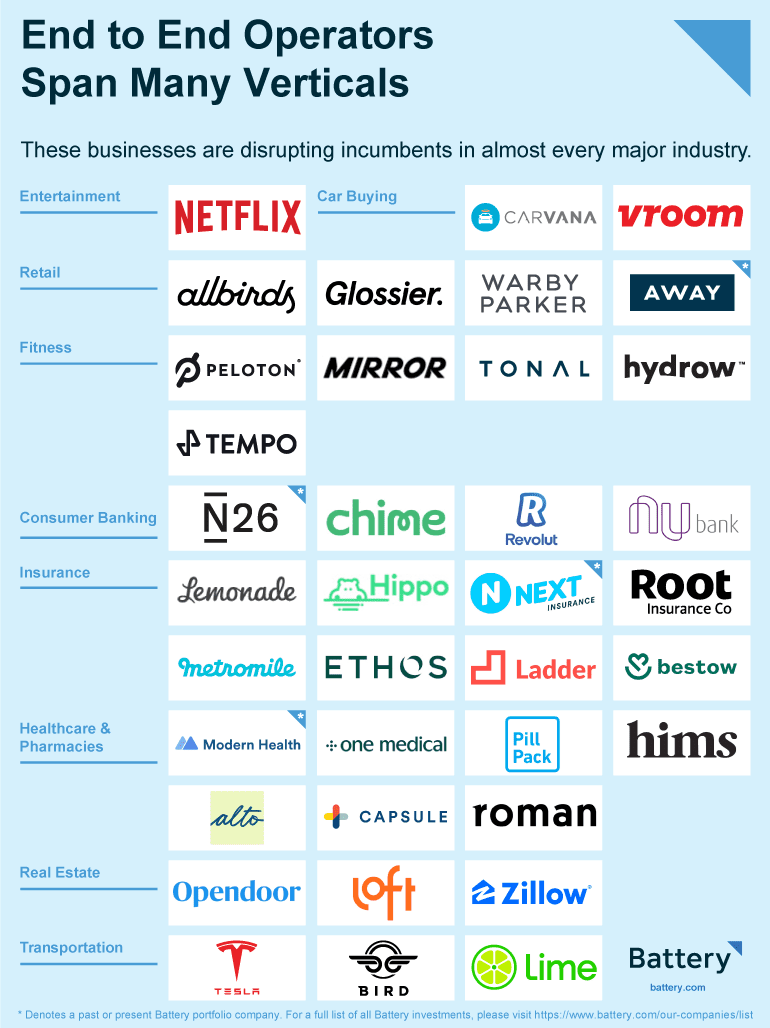

End to End Operators span many verticals

Many of these businesses have reached meaningful scale across industries:

All of these companies have recognized they can deliver more value to consumers by “owning” every aspect of the underlying product or service – from the bike to the workout content in Peloton’s case, or the bank account to the credit card in Chime’s case. They have reinvented and reimagined the entire consumer experience, from end-to-end.

What does success for end-to-end operator businesses look like?

As investors, we’ve had the privilege of meeting with many of these next-generation end-to-end operators over the years and found that those with the greatest success tend to exhibit the five key elements below:

1. Going after very large markets

The end-to-end approach makes the most sense when disrupting very large markets. In the graphic above, notice that most of these companies play in the largest, but notoriously archaic industries like banking, insurance, real estate, healthcare, etc.. Incumbents in these industries are very large and entrenched, but they are legacy players, making them slow to adopt new technology. For the most part, they have failed to meet the needs of our digital-native, mobile-savvy generation and their experiences lag behind consumer expectations of today (evidenced by low, or sometimes even negative, NPS scores). Rebuilding the experience from the ground up is sometimes the only way to satisfy today’s consumers in these massive markets.

2. Marriage of technology and data as a core differentiator and moat

Technology and data underpin all successful end-to-end operators. Working in conjunction, they have the ability to drive more efficient customer acquisition or distribution, reduce variable and fixed costs via automation, lower prices for consumers, expand or create incremental supply, and ultimately deliver better experiences (which means more loyal customers). Data and technology are what separate incumbents from the next-gen and produce deep moats over time, making it hard for new upstarts to unseat them.

Good examples where these trends are playing out are the next-gen insure-techs like Lemonade (for renters insurance; NYSE: LMND), Hippo (for homebuyers), Ethos (for life insurance), Next Insurance* (for small businesses) and Root Insurance (for autos; NASDAQ: ROOT). These companies use technology to simplify the traditionally opaque insurance-buying process and allow consumers to purchase new policies much faster and with much greater ease. As digital-only products, they don’t rely on offline agency networks for distribution like legacy incumbents do, and their customers can purchase policies wherever they are. Aggregating real-time data signals allows them to underwrite their customers more accurately, which can translate to savings (especially for lower-risk customers).

3. Superior unit economics relative to legacy incumbents

Technology should also yield superior business models for end-to-end operators. While these businesses are often more capital-intensive initially (as they require rebuilding infrastructure from the ground up, and own more pieces of the value chain), their steady-state P&Ls can be more attractive due to better unit economics and lack of overhead associated with legacy businesses.

Neobanks like Chime, N26* and Revolut are great examples. Despite eliminating fees to consumers, they still exhibit very attractive unit economics. They do this by first operating without the overhead costs of physical branches – they don’t need bricks and mortar because they’re purely digital. Their revenue model is also lucrative: For example, every time a consumer swipes their debit or credit card, the merchant pays an interchange fee of which the neobank takes a cut. That’s a predictable, consistent revenue stream with high margins. Further, consumers who set up direct deposit into their neobank accounts are much stickier. With a customer relationship this deep, they can offer services like lending, trading, or wealth management which increase average revenue per user (ARPU) with zero marginal acquisition cost.

Of course, for every success there are also failures. Take WeWork: The company certainly offered a delightful experience, but it was mis-managed and lacked a sustainable business model, with unit economics that just didn’t work. It was a great product, but a bad business. If you’re building an end-to-end business, ensure you have both.

4. Brand builds trust = organic growth

When you own and operate the experience end-to-end, you can create a delightful and enduring brand while carving out a niche unique to you. Over time, this benefits you by attracting more customers organically, through word of mouth or simply brand recognition.

Many well-known D2C e-commerce companies pioneered the end-to-end approach, with a laser-focus on building great brands. Away’s* luggage is the centerpiece of an Insta-ready brand culture around travel. Dollar Shave Club* parlayed funny, memorable ads about razors into a digital brand for all men’s grooming products. Glossier (beauty/wellness) leveraged influencers to grow their brand via social media.

Nothing good comes easy

End-to-end operator businesses aren’t for everyone. They’re challenging to build because “you need to get good at many different things: software, hardware, design, consumer marketing, supply chain management, sales, partnerships, regulation, etc.” as Chris Dixon said.

As a founder seeking funding, you may find yourself needing to over-explain to VCs all the things you are investing in, and why those extra investments will pay off over time. However, when executed correctly, these upfront investments can result in dramatically better customer experiences, hard-to-replicate businesses, superlative economics, and category-defining brands – all of which can unlock significant value over time. The right investor will recognize when you have all these elements of success and help you unlock the company’s full potential.

This article originally appeared in TechCrunch.