APE (ARR per Employee) Is the “North Star” Efficiency Metric You’re Looking For

7 min read

In a recent report, we spoke about how the market has shifted to valuing cloud companies’ profitability, even when that comes at the expense of growth (this thread on X goes in-depth on that data).

There is no shortage of efficiency metrics that cloud executives can track today to gain a better perspective on their overall economics. Sales-and-marketing efficiency metrics such as LTV-to-CAC, CAC payback, and magic number have long been mainstays in board decks and fundraising materials. As the market has turned, burn multiple (net burn / net new ARR) has emerged as a popular, all-encompassing way of looking at burn vs. ARR growth.

The difficulty with these efficiency metrics, though, is that they aren’t tangible in a way that is actionable for your employees. They feel more like financial metrics than operational ones, and it is difficult for employees to execute against these concepts in their daily activities.

Improvements in product can absolutely have a large impact on sales efficiency, but those improvements are a derivative on product and engineering work rather than something that can feel top-of-mind. Burn multiple puts the emphasis on having “less bad burn” vs. being instructive on what actions will actually drive profitability.

Our advice for cloud CEOs? At your next all-hands meeting, or during your next one-on-ones with functional leaders, align your team around ARR per employee, a metric we are calling APE.

APE stands for ARR per Employee, and it’s an extremely simple metric we think could serve as your north star as you navigate these volatile times.

Why should APE be the efficiency north star?

The cost structure of a cloud company is driven primarily by people. There are other costs to be mindful of, such as cloud expense (spending on AWS/Azure/GCP), real-estate expenses (less impactful than it used to be!) and expenditures on other SaaS applications you need to run your business. But around 70% of your costs, most likely, are going to relate directly to your employees. If you want your business to become more efficient, at the end of the day, your employee base is the place to start.

One key point here: Optimizing your employee base should ideally come through smart, measured hiring, not a reactive RIF (reduction in force). Achieving the former will help your business avoid the latter. When attempting to instill this hiring discipline across your organization, the APE north star can be a powerful tool.

As a manager or executive, every decision you make has an impact on APE. Every new initiative or project that needs to be staffed impacts APE. Every backfilled role impacts APE. If you can automate a task with software or spread new projects between team members, your APE improves. Before any personnel-related move is made, APE should be discussed.

Some key benchmarks to keep in mind

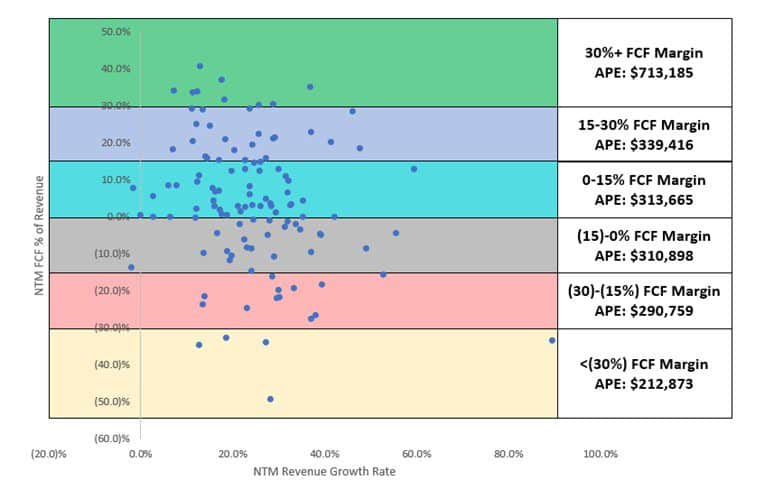

Unlike magic number, or the “Rule of 40”, there is no one APE number we recommend. The APE of a company with all employees co-located in the Bay Area, for example, needs to be much higher than a company that has employees in lower-cost geographies to reach profitability. But we can offer to some data points to help guide you, all derived from Capital IQ data and Battery research through many years scaling software businesses.

At giant and profitable tech companies like Google and Facebook parent Meta, the APE number is significantly higher than the public cloud comps: $1.7M at Google and $1.4M Meta (using MRQ revenue * 4 in the numerator as a proxy for ARR).

Meanwhile, the APE figures for smaller, privately held SaaS businesses are typically much lower. You might be a bit surprised at how far off you are from these comps. A Series B company with $5M in ARR and 80 employees would have an APE of just $63K; a Series D-stage company with $50M in ARR and 300 employees has an APE of just under $167K.

If you’re still far away from these public benchmarks, that’s OK (and normal). Based on our pattern recognition, below are the APE ranges we generally recommend targeting by ARR scale (with caveats around gross margin, geographic location, balance sheet, and forecasted growth rate):

Getting to a higher APE earlier in the maturity cycle is likely a net positive. Overall, we believe having an aspirational goal of getting to $200K would serve most mid-stage/late-stage growth companies well. That’s still not enough to be breakeven, which we discuss next.

Tracking your Breakeven APE (and why this should be in every board deck)

The calculation for Breakeven APE is “total expenses / employee.” Total expenses should include not just personnel costs, but all expenses (for example, marketing expenses and cloud hosting costs). We think that employee count is best looked at point-in-time vs. as an average over some period.

CEOs should be aware of their Breakeven APE and closely track this number. Breakeven APE can be very different across companies – we’ve seen as low as $150K and as high as $450K+. Bill.com, for example has an APE over $450K but isn’t breakeven yet on a P&L basis; Ceridian HCM has an APE of just $160K but is free cash flow positive.

We would advise not to include stock-based compensation (SBC) in this calculation, since that is a non-cash expense that does not impact cashflow breakeven. That is not to say that stock-based compensation does not matter; on the contrary, it is highly impactful in building shareholder value and often underappreciated. Breakeven APE including SBC is a much higher, but we would encourage companies to track towards the intermediate milestone of Breakeven APE excluding SBC first.

It is worth noting: Breakeven APE is on the rise for companies. Most companies are not fully aware of how fast Breakeven APE is rising on them in the current inflationary environment.

The fully loaded cost of an employee has gone up substantially over the last ten years for cloud companies. In our estimate, Breakeven APE has gone from around ~$180K a decade ago to ~$250K today, with some companies now at or above $300K. Founders should not make the modeling assumption that “total expenses per employee” is constant and that growing APE alone is enough to get to profitability. You need to actively discuss strategies to keep Breakeven APE in check over time (e.g. hiring in low cost locations, or shifting employee mix to have the appropriate level of entry employees/salaries).

At the end of the day, market leadership is still what matters

It is important that companies take a deeper look at their efficiency in the current market, but it is also important to be thoughtful around how you achieve that efficiency.

It is still important to be the winner of your market. The nature of your market matters: If you are in a highly competitive, horizontal product-market space (say, developer tooling) vs. a niche, vertical SaaS market where you feel limited competitive pressure, that can impact how you think about the correct APE your current point in the company journey.

Employee experience is still important. You want to build a company where great talent wants to work and feels supported. Culture absolutely still matters.

If you are in a position where you raised money once (or twice!) in 2021 and have years of cash in the bank, austerity likely is not prudent, but greater discipline likely is. You can drive Breakeven APE lower through automating repetitive tasks or simplifying your employee perks program (many “perk point solutions” have <10% utilization).

In Conclusion:

Our advice is to start focusing on Current and Breakeven APE today, particularly if your ARR is north of $20M.

Operational discipline was always an important muscle to build, but in a “free-capital” environment, the emphasis could wait until post IPO. In fact, in our T2D3 post from several years ago didn’t even reference the need for efficiency.

Take a look at your current APE and where your financial model puts you at the end of the year. If your model has your APE declining year-over-year, you should take a long, hard look at your model. Ideally, the company can make significant progress on APE each year.

To highlight one example of how to make this actionable: just this week, one of our pre-IPO stage companies decided to rally its entire company around getting to $200K APE. That’s almost a 25% increase from their current APE, and a great midpoint on their way to Breakeven APE.

Ultimately, your company will not be valued as a multiple of your APE, but the discounted value of your future cash flows (unless, of course, we’re talking Bored Ape NFTs!). You need to have a north-star metric that will help your team lead you there. We believe APE is the most elegant metric around which to re-orient, and it can be the center of your all-hands presentations over time. Current APE and Breakeven APE provide the near-term goal posts, and the targets in the table above can help as reference points for the next chapter of the journey.